1. Macro

After the mid-autumn Festival, global markets will welcome “Super Central Bank Week” , the Federal Reserve will hold its September meeting, and the central banks of Japan, the United Kingdom and Turkey will also announce their interest rate decisions this week, global markets may face another test.

The situation of each kind of raw materials

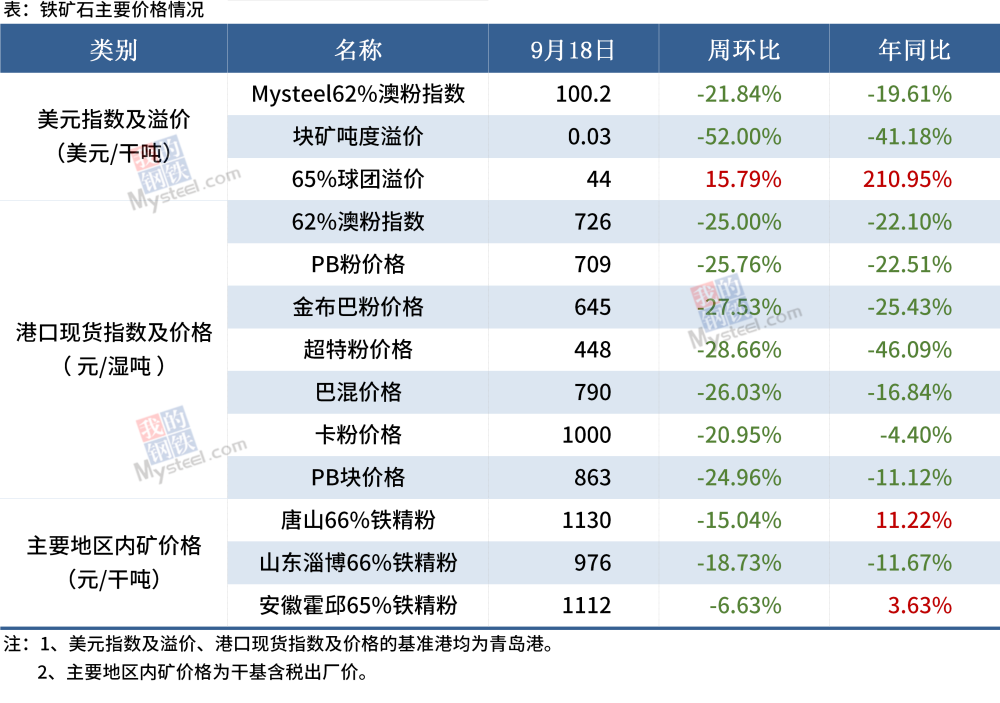

1. Iron Ore

Due to the impact of berth maintenance, iron ore shipments from Australia and Brazil are expected to drop to this year’s average level this week. Due to the impact of the typhoon early last week, arrivals in Hong Kong will also have a relatively significant reduction. On the demand side, production restrictions will continue to be strictly enforced in all regions, and there is a possibility of further tightening in some regions, and demand will continue to weaken. In addition, as the weather improves, port arrivals and unloading will gradually return to normal, iron Ore port inventory will also be reflected in the increase, iron ore fundamentals as a whole will continue to maintain excess supply pattern.

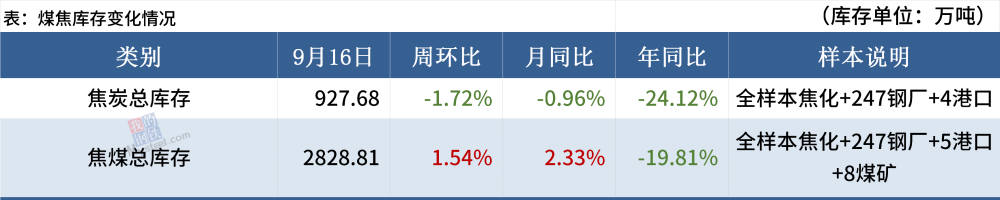

(2) Coal Coke

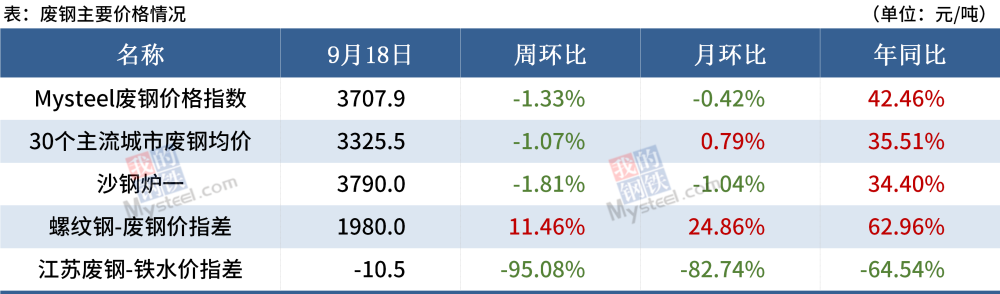

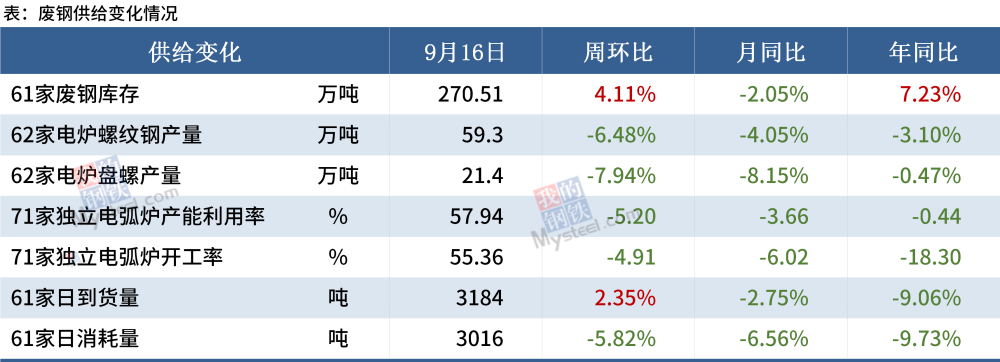

(3) scrap

From the point of view of scrap difference, scrap price is still lower than the cost of Molten Iron, scrap price is high. From the point of view of screw waste difference and plate waste difference, at present, steel mills are profitable, scrap should exist demand. However, in view of the recent multi-provincial measures to limit production continue to tighten, and even some southern provinces appear “double control” policy, leading to the overall weakening of domestic demand for scrap steel, at the same time, related varieties of ore overall decline, on the scrap steel market pressure. In addition, the current domestic resources by strict environmental protection and production of waste enterprises to reduce the impact of part of the supply of scrap market slightly boosted.

(4) billet

With the further rise of billet price, the profit space of downstream steel rolling continues to be squeezed, the single ton loss of section steel is over 100, the delivery pressure continues to exist, the enthusiasm of billet decreased significantly. At present, the pressure of billet is mainly concentrated on the downstream rolling process, which causes the trend of stock lowering to slow down. But at present billet supply remains at a low level, steel prices, and trade links in the basis of frequent fluctuations in the process of closing and selling opportunities, in addition to Tangshan short-term or there is still a tightening action on environmental protection, the price still has some support.

Situation of various steel products

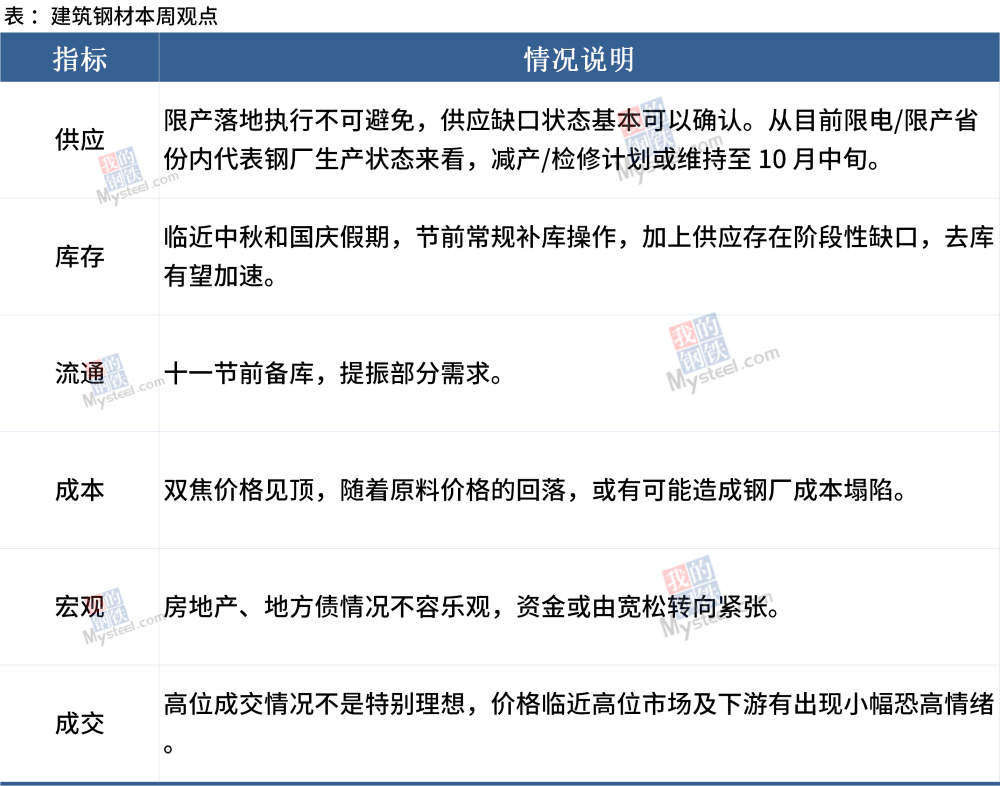

(1) construction steel

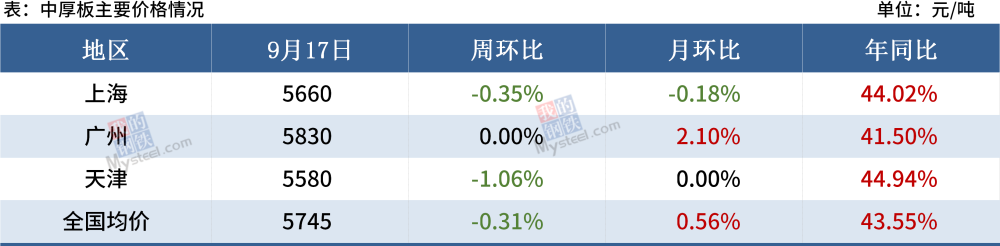

(2) medium and heavy plates

Medium plate production increased slightly last week, but overall is still at a low level, in Jiangsu production constraints, the short-term production is expected to continue to decline; recently, the north-south price gap has opened, south China is stronger than east China, north China. But from the cost measurement, the current price difference is still not enough to support the northern resources to the south; this week’s market performance, the downstream procurement slow progress, but two sections approaching, the downstream will face a round of replenishment.

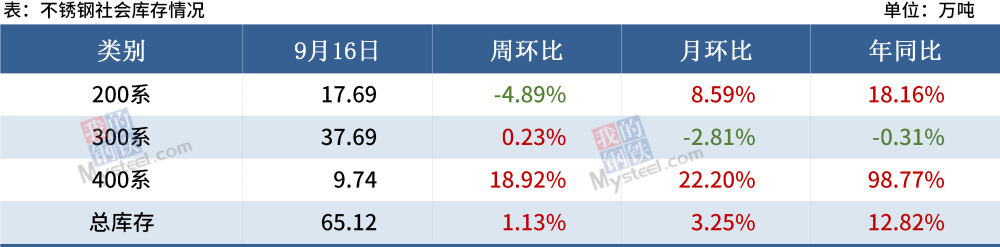

(4) stainless steel

Reduced supply expectations are still the order of the day. This round of price increases, the main driving force from the production limit to control energy consumption, that is, due to power rationing, which some enterprises production capacity and output can actually support their normal production, but the production had to be stopped because of energy consumption control. In general, the expected reduction in supply is still the main theme at present, and the September production restriction may actually affect the longer-term supply, and in the current situation where social stocks present a barrier, after the stocks are properly digested, the long-term supply-demand conflict will be even more pronounced than the current one.

Recent weakness in downstream stainless steel demand, weak domestic infrastructure investment, limited rebound in manufacturing, accelerated decline in domestic consumption and export orders, reflecting the weakening of domestic and overseas demand support. In addition, after the price increase, stainless steel economy is further weakened, facing the possibility of being replaced by other materials.

Post time: Sep-24-2021